Ask the President

The "Ask the President" section of the SinterCast website provides an opportunity for our Customers, our shareholders and the media to pose questions directly to the Company. This open access forum is intended to improve the efficiency of the information flow by allowing everyone to share in the responses issued by the Company. Review the current archive of questions and responses below.

Please submit your question (maximum length 200 words) using the following form. Your question will then be posted together with a response from the Company. Please submit each question separately. Although we will try to reply to all questions, we will continue to respect the confidence of our customers and not disclose any specific details about production commitments, volumes, or fees.

* Required fields

Previous Questions

It is certainly true that the market is low, and indeed, in the current climate, SinterCast has been quiet. However, the field activity is starting to increase and I’m more confident than ever in the long-term outlook.

Our current production is almost evenly split between commercial vehicles (45~50%) and passenger vehicles (45~50%), with off-road applications accounting for approximately 5%.

Commercial vehicle sales in Europe and the US have been low over the past year. However, year-on-year order intake improved in Europe during the fourth quarter, providing the onset of recovery. In North America, freight demand is improving and the stabilisation of tariffs and emissions regulations is expected to start to bring fleet buyers back to the market. Overall, Europe has already shown signs of recovery and most analysts expect North America to improve during the year. With our new commercial vehicle programmes continuing to ramp up, we expect our growth to outpace the overall market in 2026.

The passenger vehicle market in the US – our largest end-user market – finished at 16.3 million in 2025, an increase of 2.3% compared to 2024. The outlook for 2026 is for slight growth, with pick-ups and large SUVs – our main sectors – continuing to take increasing market share. Accordingly, the SinterCast passenger vehicle production can be expected to remain strong, with growth opportunities.

The automotive industry is currently in a low patch. We’ve weathered low patches before and we always return to growth. In the past, we have benefitted from new programmes coming on stream to allow our growth to outpace the wider market recovery. We’ll do that again this time.

A few years before Covid, I started to say that “in the fullness of time, all commercial vehicle manufacturers will adopt CGI”. This prophecy has become true. We have already frozen high volume programmes that will start production in 2027 and 2028. We are now working on high volume programmes that will start production in 2030.

The future looks bright. The challenge from electrification has faded – as we said it would. With new SinterCast-CGI engines sitting on the sidelines in China, waiting for the local economy to improve, China will start to contribute. The first SinterCast-CGI production in India is scheduled to start during the second quarter. And, in preparation for growing CGI demand, the outlook for installation revenue is positive.

The current slowdown is a frustrating delay, but it isn’t a change in our outlook. I remain totally confident that SinterCast will reach the seven million Engine Equivalent milestone in the current five year planning horizon, and that there will be growth beyond.

Ford and the UAW reached a tentative agreement late Wednesday, 25 October. As part of the tentative agreement, all Ford workers will return to their jobs and Ford’s production will return to full capacity as soon as possible. In parallel with the return to work, the UAW’s “National Ford Council” will meet in Detroit on Sunday 29 October to review the details of the agreement and to vote to send the full proposal to members. After a consultation period, it is expected that the members will vote to ratify the agreement in early-November. The new agreement would be valid until 2028.

The UAW is encouraging its members to accept the tentative agreement. In general, the agreement includes an immediate 11% pay rise and a 30% increase through 2028. The strike began on 15 September and it escalated to include the Kentucky Truck Plant – Ford’s most profitable plant – on 11 October. The Kentucky Truck plant is the main manufacturing facility for Ford Super Duty vehicles, which use the SinterCast-CGI cylinder block for the 6.7 litre diesel engine.

Fortunately for SinterCast, there has not yet been any negative impact from the UAW strike. The 6.7 litre cylinder block is cast and pre-machined at the Tupy foundry in Brazil. Thereafter, it is shipped to the Ford plant in Chihuahua, Mexico for final machining and engine assembly. The finished engines are then shipped to Kentucky for vehicle assembly. There has not been any change in the supply volume between Tupy and Chihuahua during the strike.

Let’s start with the easy one – the decision is entirely unrelated to SinterCast or the performance of our technology. It is purely a business decision by the OEM. At present, we understand that the stoppage of the foundry production will be sometime during the second half of 2024 and that the stoppage of engine manufacturing will be a few months later, due to the supply pipeline. We assume that the OEM will inform about the change after that, possibly in early 2025. In the meantime, our confidentiality obligations prevent us from saying anything about the identity of the OEM or the production details.

With regard to our series production, we’re on a really good growth path at the moment, benefitting from strong truck sales in Europe and the US, and the return to full production of the Ford Super Duty engine. With a current volume of approximately four million Engine Equivalents, we expect to maintain our double-digit growth from now until the foundry stoppage occurs. For the programme in question, there will not be a ramp down. We expect the current volume to remain constant, possibly with a slight increase toward the end of the programme to build the normal bank of spare parts for the future. Overall, the outlook is for continued growth followed by a discrete decrease sometime in the second half of 2024. From that point, we’re immediately back on the recovery and growth path.

Our smallest casting weighs approximately 5 kg and our largest casting currently weighs more than 2,000 kg. As our business model is based on the total weight of the castings shipped from the foundry, it isn’t helpful to discuss the number of castings. Therefore, in 2002, we introduced the term “Engine Equivalents” to compare our series production in an apples-to-apples way. We defined one Engine Equivalent as 50 kg, because this is the typical weight of a cylinder block in a normal passenger vehicle. When we refer to our full-year 2022 production as 3.5 million Engine Equivalents, our stakeholders can visualise the equivalent production of 3.5 million passenger vehicles – approximately ten times the number of cars sold in Sweden in 2022.

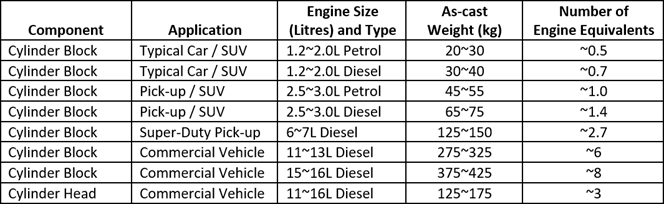

Cylinder block weights can vary quite a lot depending on how many features the OEM incorporates into the design. For example, some cylinder blocks may include extensions to enclose the timing belts at the front and to mount the transmission housing at the rear, tunnels for balancer shafts, and/or fracture split main bearings. For a typical 13 litre commercial vehicle cylinder block, these cast-in features could increase the weight of the cylinder block weight by approximately 100 kg (~30%) … but they reduce the total number of engine components, improving the efficiency of engine assembly and reducing the overall cost. Considering the variations in design strategies among the many OEMs, the typical weights for cylinder blocks and heads can be summarised as follows:

High-Silicon CGI (HiSi CGI) isn’t really a new type of CGI; it’s just a different recipe for CGI. The report in question can be found at the following link:

https://www.vinnova.se/globalassets/mikrosajter/ffi/dokument/slutrapporter-ffi/hallbar-produktion-rapporter/2017-05491sv.pdf?cb=20220705102605

Cast iron is a mixture of graphite particles in an iron matrix. The shape of the graphite particles is the same in both the conventional CGI and in HiSi CGI. The difference is in the iron matrix. In conventional cast iron, the silicon content is 2.0~2.3% and the iron matrix is pearlitic. In contrast, the silicon content of HiSi CGI is 4.0~5.0% and the matrix is ferritic. Only the iron matrix is different. The contribution of SinterCast is to control the shape of the graphite particles, and therefore, there is no difference in the foundry production requirements or in the market opportunity for SinterCast.

HiSi cast irons are not new in the industry; they have become common for many ductile iron applications over that last twenty years. There have also been several prior studies on applying the HiSi approach to CGI. In general, the HiSi alloys have the potential to provide the same levels of strength as conventional pearlitic CGI, but possibly with better heat transfer (depending on the silicon content). It is an interesting development, but more work needs to be done to define the optimal silicon content and to understand the implications for engine durability and manufacturing (machining).

High-Silicon cast irons are an active field of research shared by the automotive and foundry industries. Currently, all heavy duty CGI engine components are produced with a pearlitic iron matrix. The first HiSi applications may be realised in the 2027~2030 time period. SinterCast welcomes and supports the development. For SinterCast, there is no preference between conventional pearlitic CGI and HiSi ferritic CGI.

The Impro production complex in Mexico, with five manufacturing facilities, has been established to: expand the global footprint of Impro Industries; to better serve the Impro customers in the Americas; and to avoid the tariffs that are currently imposed on metal components between China and the USA. As stated in the press release, the first CGI component to be produced at the Mexican foundry will be the transfer of an existing SinterCast-CGI component that is currently being produced at the Impro foundry in China and exported to the US. Impro estimates that the total production capacity of the new foundry will be 60,000 tonnes per year of shipped castings, including grey iron, ductile iron and CGI components. The production mix will depend on the transfer of programmes from the Impro foundry in China and the receipt of new series production orders. While the initial CGI volume will be modest, we are confident that it will grow as the market demand for CGI continues to develop. Considering the diverse range of components traditionally produced by Impro – including suspension, structural and safety components – it is likely that the foundry will maintain a mix of ductile iron, grey iron and CGI, but there are no technical reasons that would limit the CGI volume.

Many apologies for the inconsistency between the English and Swedish reports. The opportunity for the FAW 16L engine is for the cylinder block. Each cylinder block will provide approximately seven Engine Equivalents, making the FAW 16L a high volume opportunity.

We are currently working on the development of a handful of new concepts and products. Some of these are extensions to our Tracking Technologies, and some of these have the potential to be offered to the market as stand-alone products – without the need for a Tracking installation. We are also leveraging our core competence in cast iron thermal analysis to investigate other thermal analysis products that can help to improve the understanding of the behaviour of the iron – and thus reduce scrap rates – in the foundry. My old PhD supervisor used to say that development is like photography: “from a roll of 36, you hope to get one or two good shots.” We are constantly developing, and some of our current projects are quite promising. We hope to introduce new functionality and new products to the market as we move forward.

In response to the movement toward zero emission transportation, commercial vehicle manufacturers are investigating several different powertrain technologies. These include battery electric vehicles (BEVs), fuel cells, and internal combustion engines (ICEs) based on a variety of potential fuels, including biodiesel, e-gas, synthetic fuels (OME and DME), natural gas, ammonia, and hydrogen. With European legislation requiring the sale of initial volumes of zero emission trucks before 2025, many OEMs will begin by offering BEVs. But the volumes will be small and the initial technology display will not affect the overall market demand.

The push for zero emissions is linked to the international climate agreements and the European ‘Green Deal’ for carbon neutrality in 2050. The volume phase-in of new commercial vehicle technologies is not expected before 2040. Both Bloomberg and IHS Markit (a leading automotive analyst) predict that heavy-duty commercial vehicle sales in the US will still be 80% diesel in 2040. In the meantime, it is still too early to know which technologies will prevail.

Most industry insiders believe that battery electric vehicles will be suitable for short haul and ‘last-mile’ delivery trucks, where the vehicles can return to a depot every day for recharging. But there is less confidence in BEVs it for long haul trucking. For long haul, most OEMs are investigating liquid fuels because liquid fuels combine higher energy density with the potential for zero emissions (or ‘zero-impact’ emissions, where the CO2 and NOx emissions are lower than the ambient air quality). The path for the use of liquid fuels in ICEs is attractive because it has the potential to satisfy carbon neutrality while enabling the industry to maintain the mature infrastructure investments and expertise for engine manufacturing.

In parallel with the investigation of BEVs, hydrogen is also receiving a lot of attention. But it is not yet clear how the hydrogen will be used – will it be in an internal combustion engine (ICE) or in a fuel cell? If the hydrogen is used in an ICE, the market opportunity for SinterCast will be the same as diesel.

The market will evolve, but it is still early days. In the near-term, it is clear that the demand for performance, fuel efficiency and emissions in commercial vehicles will become more stringent. This demand will require further increases in engine loading and it will increase the opportunity for CGI. For SinterCast, we regard commercial vehicles as our largest growth opportunity. We continue to regard commercial vehicles as a growth opportunity well-beyond 2030.

The decrease in Sampling Cup shipments is due to reduced production of exhaust components at the Dashiang foundry in China. There are several factors to consider in the production of exhaust components:

- The weight of each component is approximately 5 kg; the typical weight for cylinder blocks and heads is 50~300 kg

- Exhaust components are produced from small ladles (~750 kg); the typical ladle size for cylinder block and head production is ~2,000 kg

- The mould yield for exhaust components is ~30% because of the relatively large amount of filling channels needed to feed the iron into the individual pieces in the mould; the typical mould yield for cylinder block and head production is ~70%.

Taking all of these factors into consideration, the production of exhaust components consumes approximately five times more Sampling Cups per Engine Equivalent than the production of cylinder blocks and heads.

The CGI exhaust manifolds produced by Dashiang are primarily used in small (<2 litre) diesel engines used in European passenger vehicles. The demand for these engines has recently decreased, and therefore, the Dashiang production has also decreased. During the first half of the year, the year-on-year Dashiang volume was down by less than 20,000 Engine Equivalents, so there was almost no impact on the series production volume.

The impact on Sampling Cups appears larger for two reasons. First, the five-fold higher consumption rate. Second, the reported Sampling Cup volume is based on ex-works shipment from SinterCast – not on customer use. Dashiang placed a large order for Sampling Cups in late-2018 and they continue to consume from that stock – there have not been any Sampling Cup shipments to Dashiang thus far in 2019. Therefore, the reported Sampling Cup volume in 2018 was higher than normal and the Dashiang volume thus far in 2019 is zero; even though thousands of Sampling Cups have been consumed this year.

In summary, the production volume and thus the Sampling Cup consumption are lower at Dashiang, but it does not have any significant impact on the overall series production, or on the overall growth outlook.

The quarterly CEO interviews were a part of the service provided by Remium and Introduce. After the acquisition of Remium by ABG Sundal Collier, SinterCast has decided to adopt the new format offered by ABGSC. SinterCast continued with the quarterly audio interviews until the end of the 2018 financial reporting, and the last interview was published in conjunction with the 4Q18 interim report on 20 February 2019.

Going forward, SinterCast will participate in two ABGSC Small Cap events per year, providing a market update presentation followed by a CEO video interview. The presentations and the interviews will be available on the ABGSC and SinterCast websites. The first ABGSC video interview was conducted on 13 March 2019 (watch the interview). The next ABGSC presentation and CEO video interview is scheduled for early December.

Overall, the new format will provide a broader frequency of information from SinterCast. Instead of four information events per year, there will now be six, with two of the events providing additional information in between the regularly scheduled interim reports.

The EPA initially issued a Notice of Violation against FCA on 12 January 2017. FCA immediately stated that there was no malfeasance and that it would defend the claims. Since that time, FCA has worked with EPA and CARB to identify solutions. In parallel, the production of the 3.0 litre V6 diesel engine for Jeep and Ram vehicles has been suspended. On 19 May, FCA issued a press release to state that a technical resolution had been agreed and that it has applied to EPA and CARB for approval to begin selling Model Year 2017 vehicles with the 3.0 litre V6 diesel engine. On 23 May, the EPA issued a press release stating that it will seek civil penalties for the Model Year 2014-16 engines that it claims to be noncompliant. FCA has responded to the EPA court filing in a further 23 May press release stating it is “currently reviewing the complaint, but is disappointed that the DOJ-ENRD has chosen to file this lawsuit. The Company intends to defend itself vigorously, particularly against any claims that the Company engaged in any deliberate scheme to install defeat devices to cheat U.S. emissions tests”.

For SinterCast, these are two separate issues – the past and the future. Regarding the past, the US courts will need to decide if a penalty will be levied against FCA for the model year 2014-16 engines, and if so, the amount of that penalty. SinterCast is only an observer in this. Regarding the future, the Model Year 2017 diesel vehicles are undergoing a separate approval process, where it has been stated that a technical solution has been agreed. SinterCast can therefore expect an increase in the FCA 3.0 litre V6 diesel production, as Model Year 2017 Jeep and Ram diesel vehicles return to showrooms.

Volkswagen acknowledged that it installed so-called “defeat devices” to intentionally alter the performance of the emissions control systems in its diesel vehicles. As a result of this, the EPA announced in 2015 that it would conduct more detailed evaluations of diesel vehicles. The EPA’s detailed evaluation of the FCA 3.0 litre diesel has identified operating conditions where the NOx emissions levels are higher than expected. The EPA therefore issued a Notice of Violation to FCA on 12 January. The Notice of Violation did not claim that that any defeat devices had been implemented. FCA has provided an initial comment to state that it has complied with the emissions legislation and that it has not implemented any defeat devices. At this point, we believe that FCA should be given the time to study the allegations and provide a formal reply before any conclusions are drawn.

The recent discussions about diesel engines and emissions legislation has not affected the announcement and introduction of new diesel models in the United States. General Motors has introduced diesel engine options in the Chevy Cruze, the Chevy Colorado and the GMC Canyon and Ford announced the introduction of a diesel engine option for the F-150 on 9 January 2017. Volkswagen’s affiliate brands, Audi and Porsche, have also indicated that they will re-introduce diesel engine options after the current settlements and technical fixes are resolved. Together, these actions shows a strong commitment toward diesel as a part of the future product mix.

At this stage, it is not possible to determine how future emissions legislation will be formulated and how these legislations will influence diesel take rates. SinterCast will follow this development as it continues to support the development and production of all types of engines, for passenger vehicles, commercial vehicles, and industrial power applications.

At present, there are only two V-diesel engines in the market that are not based on CGI cylinder blocks: the Mercedes 3.0L V6 (aluminium) and the General Motors 6.6L Duramax V8 (grey cast iron). CGI has effectively become the standard material for V-diesel engine cylinder blocks. SinterCast has consistently said that it is possible to produce a cylinder block in any material: grey iron, CGI or aluminium – the ultimate difference is in the size and the weight of the engine. If the material is weaker, the walls of the cylinder block must be thicker to ensure durability. This impacts size, weight, packaging and crash impact. We believe that CGI provides the best overall solution for V-diesel engines.

Engine design is a complex science with many different factors determining performance and durability. One of the specific features of the Duramax V8 is that the stroke is relatively short. The stroke of the Duramax V8 is 3.95 inches (100 mm) while the stroke of the Ford Power Stroke V8 is 4.25 inches (108 mm). The shorter stroke in the Duramax allows performance to be achieved through rpm and places less emphasis on increasing the combustion pressure. As the combustion pressure is decreased, the mechanical load on the materials is also decreased. The shorter stroke in the Duramax engine is therefore an influencing factor in the use of grey iron for the Duramax cylinder block.

The use of induction hardening is a common technology in metallurgy that can be applied to all types of cast irons and steels. Induction hardening heats the surface of the iron for a few seconds and then allows the surface to cool. This rapid heating and cooling increases the hardness on the surface of the material, to a depth of approximately 0.2 mm. Induction hardening can be included as an extra step in the manufacturing process to improve wear resistance – it does not provide any strength benefits to the material or to the component. Induction hardening is commonly used in the valve seats of grey iron cylinder heads to minimise valve seat wear, and for many other wear components. In the absence of detailed information, it can be assumed that the induction hardening in the Duramax engine was applied in the ring reversal area at the top of the cylinder bores (a span of approximately 25 mm, approximately 25 mm below the top surface of the cylinder bores). CGI is harder than grey iron and also has superior wear resistance (this also explains why the machining of CGI is more difficult than grey iron). None of the current production CGI cylinder blocks require induction hardening.

SinterCast has a good rapport with the Duramax design team. We wish them success with their new upgrade and welcome the opportunity to work together with them at some stage in the future.

The sale of 3,500 shares is a short term sale for the purpose of rearranging my personal holdings – it isn´t in any way related to SinterCast. I have the intension to re-purchase 3,500 shares soon to maintain my total holding.

The Environmental Protection Agency (EPA) issued a Notice of Violation (NOV) to the Volkswagen Group on 2 November 2015. Based on ongoing tests being conducted by the EPA and other agencies, the NOV stated that the engine control software resulted in different NOx emissions levels during testing and on-road driving. Volkswagen issued a press release on 2 November to state: “Volkswagen wishes to emphasize that no software has been installed in the 3-litre V6 diesel power units to alter emissions characteristics in a forbidden manner.” Independent reports published since the EPA’s 18 September NOV against the Volkswagen 2.0 litre have also shown that the emissions from the Volkswagen 3.0 litre V6 are not different from those of diesel engines manufactured by other vehicle brands.

As with the 2.0 litre diesel, the EPA claims are related to the engine control software. SinterCast does not have any additional awareness of the control software. The current investigations into diesel engines are not related to the cylinder block or the cylinder block material. It is still very early in the investigation process and it is judged that we need to wait to see how the situation will be resolved.

As stated in our 22 September Ask the President, the Audi 3.0 litre V6 sales in the US account for approximately 1% of SinterCast’s current production, so any impact on Volkswagen group sales in the US will be insignificant for SinterCast. We remain confident in the benefit of diesel engines in US pick-up trucks and SUVs and we regard this market as a continuing growth opportunity for SinterCast.

The Environmental Protection Agency (EPA) in the US filed a “Notice of Violation” against Volkswagen on 18 September. The notice claims that Volkswagen installed software that changed the engine exhaust management system when emissions tests were being conducted. Specifically, it is claimed that the software detected when the emissions testing equipment was connected to the vehicle and operated the emissions control system at full mode to ensure clean emissions results. However, when the vehicle was running on the road, the software reduced the emissions treatment causing the vehicle to emit more NOx emissions. It seems that this was done in order to improve fuel economy and to reduce the urea consumption used in the SCR exhaust treatment.

Volkswagen issued a press release response earlier today, 22 September. The response states that the software only affects the 2.0 litre diesel engine and does not affect any other Volkswagen engines or vehicles. The 2.0 litre engine is not a SinterCast engine. The SinterCast 3.0 litre V6 diesel engine manufactured by Audi and used in Audi, Porsche and Volkswagen vehicles is not implicated in the EPA Notice of Violation.

It is clear that diesel engines can meet the current US emissions legislation (which are more stringent for NOx than the current European emissions legislation). It is also clear that this exposure will result in a loss of trust for Volkswagen and will draw negative publicity to diesel engines in the US. However, there will also be many strong voices in the US that remind consumers that this is an issue of management decisions rather than an issue of the cleanliness of diesel engines. The likely outcome will be a fine against Volkswagen (VW has set aside a provision of EUR 6.5 billion). At this stage it is not possible to predict how it will affect Volkswagen sales.

The Audi 3.0 litre V6 sales in the US account for approximately 1% of SinterCast’s current production, so any impact on Volkswagen group sales in the US will be insignificant for SinterCast. We remain confident in the benefit of diesel engines in US pick-up trucks and SUVs and we regard this market as a continuing growth opportunity for SinterCast.

The series production revenue includes revenue from the Production Fee, consumables and software licence fees. The reason for the difference between the first quarter and the second quarter is simply the difference in the timing of the shipment of consumables. During the first quarter, approximately 15% more Sampling Cups were shipped than in the second quarter. In parallel, the shipment of the consumable Thermocouple Pair (which is usually ordered together with Sampling Cups) was also higher in first quarter. This increase in the consumable volume buoyed the first quarter production revenue. The series production in the second quarter was 10% higher than the first quarter and the revenue from the Production Fee increased accordingly. The difference is purely due to the timing of consumable shipments – there has not been any change in the Production Fee pricing or business model.

Since 2008, Remium has published quarterly analyst reports for SinterCast. In 2013, we decided to conduct a parallel trial with Penser, having two analysts in Sweden. We have now reviewed the analyst coverage and concluded that, although Penser has made good contributions, the incremental value of a second analyst in Sweden didn’t justify the added costs. We have decided to focus on Remium as they also support our quarterly CEO interviews and provide the liquidity guarantee service. We have enjoyed the collaboration with Erik Penser Bankaktiebolag and appreciate their publication of quarterly analyst reports. Going forward, we will focus on Remium in the home market and investigate possibilities for further coverage outside of Sweden.

It may be easier to start with the similarities between the two systems. Both systems use the same software and the same Sampling technology. Therefore, the metallurgical capability and accuracy is the same. This metallurgical commonality also allows customers to seamlessly upgrade from the Mini-System 3000 to the full System 3000.

The Mini-System 3000 was developed to provide a low entry barrier for new foundries to adopt the SinterCast technology. It is based on a simplified hardware platform and was intended for product development and niche volume production. The Mini-System 3000 does not have an automatic wirefeeder. Therefore, the foundry needs to note the corrective additions of magnesium and inoculant wire from the operator display screen and manually enter the additions into a separate manual wirefeeder. This manual step is inconvenient and not practical for high throughput applications. The manual wirefeeding also means that there is no automatic data log of the actual wire additions for quality traceability. Finally, the Mini-System 3000 is built on wheels so it can easily be moved in and out of the hostile foundry environment when it is not needed. The full System 3000 provides more robust hardware, automatic wirefeeding and full traceability for each ladle. The full System 3000 is also expandable to incorporate multiple sampling and correction stations, and also to include an additional wirefeeder for automatic base treatment. This is the basis of the System 3000 Plus.

There is not set rule as to when a foundry would need to upgrade to a full System 3000. It depends more on the ladle throughput than on the number of Engine Equivalents. For example, if a foundry processes one 10-tonne ladle per hour to make large industrial power castings, many Engine Equivalents could be produced per year even though the demand on the SinterCast system is low. In general, if the throughput exceeds a few ladles per hour, or if the end-customer demands automatic traceability, the foundry should opt for a full System 3000.

The reporting of the Production Fee has been well established over the last 15 years. Customers report the production on a monthly basis and the majority of reports are received on time. SinterCast’s Finance and Administration team has good contact to each customer and the initial follow-up of tardy reports is made on a personal level. In the event of longer delays, the responsible sales person or the local country manager can also follow up. In practice, there have not been any significant problems with timely and accurate reporting.

The production reporting is largely an honour system. However, there are checks and balances. The primary check is via the ladle-by-ladle production records in the computer of the SinterCast process control systems installed in the foundry. Every month, SinterCast downloads and reviews the production statistics at each customer and generates a “Benchmarking Efficiency Report” to provide recommendations for process optimisation. If there is a divergence between the number of ladles treated by the SinterCast system and the volume reported by the foundry, a follow-up enquiry can be made to the customer.

In the event of an ongoing divergence between the SinterCast production records and the reported volume, the contracts provide for SinterCast to request a production certificate from an auditor. However, in our experience, there has never been a significant problem with the accuracy of the production reporting. Indeed, our routine checks have identified a few errors over the years and these cases have been quickly and positively resolved.

Overall, we understand that reporting errors can be made, but we have no reason to be concerned about the integrity of the reporting. The process works well and the customers understand that SinterCast has ladle-by-ladle documentation of the production. Based on past experience and the current outlook, we don´t see any need for changes or additional administration in the future.

Materials selection for engine design is a vast and complicated subject, including technical, environmental, economical and even emotional considerations. It is therefore difficult to provide a simple answer to such a complicated question. Overall, the benefits of using CGI in a petrol engine are predominantly the same as in a diesel engine: package size; power; durability; well-to-wheels energy reduction; and, cost. The challenge, however, is that the peak firing pressure in petrol engines is lower than in diesels, so conventional grey cast iron and aluminium alloys can still offer sufficient durability for many applications. Many of the material decision factors are addressed in our engine design publication: Compacted Graphite Iron - A New Material for Highly Stressed Cylinder Blocks and Cylinder Heads

CGI is approximately 75% stronger, 50% stiffer and twice as durable as the aluminium alloys used for engine applications. These superior properties mean that engine designers can specify thinner walls in CGI, reducing the overall size of the cylinder block. In general, a CGI cylinder block could provide reductions of 10% in length, 5% in width and 5% in height in comparison to aluminium. This size reduction has many potential advantages, including (i) secondary weight savings because the components that span the length of the block (for example, cylinder heads, crankshafts, camshafts, fuel rails, etc) also become 10% shorter, and therefore lighter, (ii) easier packaging in the engine compartment, and (iii) less 'bridging' of front-end crash impact into the passenger compartment. This length advantage is more apparent in V-type engines, because V-engines benefit from the length and weight reductions on two cylinder banks.

As engine downsizing continues, and particularly as the use of turbocharging continues to increase, the mechanical load in petrol engines will increase. This can lead to a condition where stronger materials are needed to satisfy power, durability and package size requirements. If designers continue to use aluminium, the walls must become thicker, making the engine larger and heavier. This has already proven to be the case for V-diesel engines, where the Audi 3.0L V6 CGI diesel is 20% shorter and 8% lighter than the Mercedes 3.0L V6 diesel. It is therefore logical to assume that the initial CGI petrol applications will also be for V-type, turbocharged engines, due to the more challenging mechanical loads and the packaging benefits. In general, for engines where cylinder block durability is the rate-controlling-step, CGI petrol engines could be expected to provide approximately 20-30% more performance and approximately 100% more durability.

However, many non-technical factors influence in engine design. For example, if an OEM primarily uses aluminium for its existing petrol engines, it will take more effort, and competitive benchmarks from rival OEMs, to convert to CGI. This is because the casting, machining and assembly facilities are already in place for aluminium, and the competence of the design and manufacturing personnel are already aligned with aluminium. In such cases, a change of materials is a bigger and more expensive step. SinterCast must therefore concentrate its initial petrol efforts on the many OEMs that traditionally use iron.

Finally, economics and environmental considerations also influence materials decisions. In general, a CGI cylinder block will be approximately 50% less expensive than an aluminium cylinder block, and the well-to-wheels environmental profile of iron is more energy efficient than aluminium. It is true that a lighter engine can save fuel during the lifetime of the vehicle, but the energy required to produce aluminium is much higher than the energy required to produce iron. Indeed, it is not clear that the fuel savings provided by an aluminium engine over the life of the vehicle can payback the initial energy penalty. However, governments only regulate tailpipe emissions, with no regard for upstream energy consumption, and this motivates OEMs to prioritise vehicle weight over cost or life cycle energy efficiency. This is a frustrating oversight of legislators and SinterCast continues to educate and campaign for well-to-wheels accounting.

Engine designers will always prefer stronger materials, and this is the primary advantage for CGI. SinterCast has already announced that the first high volume CGI petrol engine has been approved for production and we believe that the launch of this engine will provide a new benchmark for performance, power-to-weight and energy efficiency. Our efforts to establish a first CGI reference in the petrol sector have been successful and we now look forward to the launch of this engine to increase the CGI awareness throughout the industry, establishing a new benchmark in the petrol sector, and providing further growth opportunities for SinterCast.

This question refers to a recently published study by the International Agency for Research on Cancer (IARC), based in the United States, dealing with the classification of exhaust emissions from petrol and diesel engines. The IARC study has reinforced a long-standing link between particulate emissions from diesel engines and lung cancer. However, the IARC conclusions are based on emission profiles from engines built in the 1990’s and the early part of the last decade. Accordingly, the results of the study represent obsolete engine technology used before particle filters were introduced. This fact was acknowledged by the IARC in its report.

The European Association of Automotive Suppliers (CLEPA) has issued a response to the IARC study stating:

“The IARC study does not reflect the advances in diesel emission technology in the past decade and cannot therefore be accepted as basis for regulatory or vehicle development actions. Instead of creating uncertainties in the markets, we should first complete ongoing studies on the emissions and health impacts of modern diesel engines that are equipped with the European world leading emission reduction technologies.”

Diesel technology has advanced considerably and the improvements in diesel emissions have been widely accepted by governments and regulating bodies. In April 2012, the Advanced Collaborative Emissions Study published by the US Health Effects Institute, suggested "few biologic effects to diesel exhaust exposure." These findings were presented to the California Air Resources Board (CARB) and the US Environmental Protection Agency (EPA). Currently, the EPA’s own data indicates that diesel emissions account for less than six percent of all particulate matter in the air. Today, in Southern California, more fine particles come from brake and tire wear than from diesel engines.

As a member of the United States Coalition for Advanced Diesel Cars (USCADC), SinterCast is involved in the dialogue with CARB, the EPA and US legislators. The USCADC will provide a critique of the IARC report to ensure that policy decisions are made on the basis of factual and current information. In the meantime, it is unfortunate that the media has sensationalised and cherry-picked the IARC report. However, the report is not expected to influence consumer acceptance of diesel engines in the US – the dealers who sell new diesel vehicles will quickly dispel any concerns regarding the data collected from older vehicles.

Tupy initially announced the construction of a new cylinder block and head facility in Joinville, Brazil in early 2008, and publicly stated that the new line would be used for CGI production. However, the subsequent planning was influenced by several factors. The first of these was an extended postponement in construction due to the economic downturn in 2008 and 2009. The downturn also affected the production planning for some high volume CGI engines that both Tupy and MAG referred to as guest speakers at the SinterCast AGM of 2007, resulting in a change of the expected grey iron / CGI product mix in the Tupy order book. Finally, during the construction of the facility in Brazil, Tupy entered into negotiations to acquire the Cifunsa Diesel and Technocast foundries in Mexico. Tupy’s acquisition of these cylinder block and head foundries was concluded on 18 April 2012, increasing its total capacity and establishing a production base in the NAFTA region. In consideration of these changes, Tupy decided to start the production at its new Joinville facility in grey iron, while allocating its CGI production demand to three other lines, two of which are in Brazil and one in Mexico. The decision by Tupy affected SinterCast’s installation planning, but it does not in any way affect the series production volume or revenue. Tupy continues to plan further expansions of the new facility in Joinville and, building on our close rapport with Tupy, we continue to work together with them to support their current and future CGI production requirements.

Yes, the Navistar PurePOWER foundry in Indianapolis is the "undisclosed international" cylinder block and head foundry that was referred to in the Interim Reports. For strategic reasons, Navistar required that SinterCast could not inform the market about the installation or the series production until now. We honoured this customer demand and secured the understanding of the NASDAQ OMX stock exchange. In parallel, we decided to include the installation and start of production milestones in the Interim Reports to reflect our good market progress. We are pleased that the Navistar heavy-duty cylinder block production has successfully ramped up and we appreciate the support of Navistar in issuing the joint press release.

The Board of Directors used the authorisation given at the 2011 AGM to compensate the employees in cash instead of exercising the options for 60,000 new shares in the stock market. In consideration of the current market conditions and the daily turnover, coupled with the dilution effects and administrative costs, the Board preferred to follow the AGM authorisation and to compensate the employees in cash. The cash alternative resulted in a cost of SEK 0.3 million, including social contributions. The costs will be accounted for during the fourth quarter of 2011.

With the start of a new year, the management and the Board decided to revise the format of the Interim Reports. The most significant change is that the forecast information (previously provided at the top of page 2) has been moved to the first paragraph of the report. There are two reasons for this. First, based on feedback from investors and analysts, it was clear that many people found it difficult to understand the format and content of the volume outlook table. Second, we have frequently been told that most investors do not read beyond the bullets and the first paragraphs of the report, so many potential investors never saw the table on page 2. It was therefore decided to change to a simpler narrative format and to put the important outlook information at the very beginning of the report. The intention for future reports is to simply update the first paragraph so the outlook information is available up-front, in an easily understood format.

The information previously provided in the outlook table is maintained in the first paragraph of the report. The only difference is that the ‘development pipeline’ is provided as a single number rather than as separate volumes for ‘secured orders’ and ‘development’. We feel that this change helps to simplify the report, as the previous table anyway didn’t provide a timeframe for the secured orders to be announced or launched into production. Indeed, it was common that programmes in the ‘development’ category could leap-frog programmes in the ‘secured’ category, depending on changes in OEM planning. As SinterCast has evolved from the development phase to a profitable company, we feel it is better to combine the two categories, and to rely on press releases to announce when specific programmes enter series production. Again, this should result in clearer information being provided to the market.

The other change is that the potential revenue is not included in the first paragraph. However, the revenue per Engine Equivalent is a well-known and frequently reported figure in SinterCast’s literature. Accordingly, it continues to be an easy extrapolation to monetise Engine Equivalent outlook. The revenue per Engine Equivalent is included in the ‘Business Model’ section of the Annual Report, and a new section has been added to the Interim Report to explain the business model and the clearly state the revenue per Engine Equivalent.

Finally, with regard to the deferred tax asset table, we will continue to provide the deferred tax asset information in future reports. However, because the total pool of 4.35 million Engine Equivalents presented in the 1Q11 Report had not changed relative to the 4Q10 Report, there was no change in the deferred tax asset for the period. This was simply noted in the concluding sentence of the “Results” section, rather than devoting an entire section to an unchanged result.

We realise that the revised format of the quarterly report represents a change, but we hope that the format is improved and that the outlook information will be more accessible and easier to comprehend for a wider audience.

Although the year-end liquidity was SEK 40.3 million, much of this capital was derived from the new share issue in September 2009, the shareholder warrants in October 2010, the first 15% of the employee stock option programme in December 2010, and the outstanding bank loan in the amount of SEK 3.0 million. The dividend of SEK 0.5 per share corresponds to a payment of SEK 3.5 million to the shareholders, and represents 140% of the 2010 cashflow (SEK 2.5 million)*. In deciding the amount of the ordinary dividend to be proposed to the AGM 2011, the Board considered the cashflow from operations and investments together with other factors, such as the year-end accounts receivable, the need to replenish stock following the shipment of the System 3000 equipment, and the repayment of the bank loan. The Board’s intention is to continue to provide an ordinary dividend to the shareholders, and for this dividend to grow as the business and cashflow result evolve. The Board is committed to safeguarding the liquidity of the company and, in the event that the Board considers that the cashbox exceeds the requirement of the company, the Board has the option to propose an extraordinary dividend or a share buy-back to adjust the liquidity.

*Includes cashflow from operations of SEK 3.0 million and investing activities of SEK -0.5 million

Apologies, the 30 September 2010 volumes were updated to reflect the current internal forecast, but the revenue figures were not updated. The correct table should be as follows.

|

Approximate Annual Production Potential and Revenue |

||||

|

30 September 2010 |

30 June 2010 |

|||

|

Activity |

KEQVS* |

MSEK/yr** |

KEQVS* |

MSEK/yr** |

|

Current Series Production |

1,100 |

25 |

950 |

22 |

|

Potential Mature Volume |

1,350 |

31 |

1,300 |

30 |

|

Production Orders Secured |

450 |

10 |

400 |

9 |

|

Development Pipeline |

2,500 |

58 |

2,500 |

58 |

|

Near-term Market Opportunity |

4,300 |

99 |

4,200 |

97 |

We have discussed this error with Stockholmsbörsen and it has been agreed that we will post this correction on the SinterCast website. The error does not result in a material change in the overall results presented in the 3Q Report and therefore the Report will not be revised or reissued.

My initial reaction is that this change in the near-term market opportunity should not be regarded as significant. The published value of the near-term market opportunity is a direct result of the net calculation generated by SinterCast’s internal 5-year forecast, and is not a subjective indication of the market development or recovery.

The internal 5-year forecast includes estimated volumes for programmes that are in already in series production, plus known programmes that are still in the development phase. The start-of-production dates, ramp-up rates, mature volumes and probability factors are updated for each programme every quarter, as new information becomes available. The change presented in the 1Q10 Report reflects a combination of minor adjustments in several programmes, plus a truncation (‘rounding’) effect. The change from 4.3 to 4.1 million Engine Equivalents is less than 5%, and changes on this order should be regarded as normal ‘needle-quiver’ in a 5-year forecast, especially as the industry progresses through a market recovery.

I would also like to note that the Near-Term Opportunity result published in each of the 1Q09, 2Q09 and 3Q09 Interim Reports was 4.1 million Engine Equivalents, and therefore equal to the 1Q10 Report. This suggests that the 4Q09 Report was the one that was by affected adjustments and truncation – not the 1Q10 Report.

Finally, with regard to the reference to the automotive industry recovery, SinterCast’s internal 5-year forecast does include provisions for market recovery, based on published market research. Given that a recovery factor is already included in the near-term market opportunity, it is unlikely that a current increase in vehicle sales (global sales – not specifically SinterCast-CGI vehicles) will have sufficient weight to influence SinterCast’s total production pool over the 5-year period of the forecast.

In consideration of our Chairman’s confidentiality obligations to Fouriertransform, there has been no prior discussion between Ulla-Britt Fräjdin-Hellqvist and SinterCast in this matter. Ulla-Britt contacted me today immediately after the Fouriertransform press release was issued to ensure that SinterCast was aware of the investment. Ulla-Britt has confirmed that, due to her role with SinterCast, she has not participated in any of the discussions or decisions related to NovaCast. This has also been confirmed by Fouriertransform.

I would like to begin by putting the question into perspective. The Gandhara transaction isn’t directly about its shareholding in SinterCast. Rather, Gandhara made a voluntary decision to close its entire hedge fund and return the invested funds (approximately USD 2.3 billion) to its investors. The SinterCast shares represent less than 0.1% of the total Gandhara fund.

Over the past months, Gandhara has divested its holdings in a controlled manner and, in parallel, has sought a placement for the SinterCast shares. Gandhara has now succeeded to place the shares with a new nominee shareholder, in an off-the-market placement. SinterCast does have direct contact with the new nominee shareholder and I can confirm that the new shareholder believes in the SinterCast technology and has a long term perspective on the SinterCast investment. For SinterCast, the transaction is successfully concluded, with a new and supportive major shareholder, and we continue to focus on the core business.

In closing, I would also like to take this opportunity to thank Gandhara for its longstanding support of SinterCast and its cooperation in placing the SinterCast shares.

I would like to begin by stating that we share the frustration of our shareholders. Despite some delays in the targeted new System 2000 installations, we were pleased with the overall development of our business during 2008, and particularly with the second half of the year. In September, we achieved record annualised production of 750,000 Engine Equivalents, a 65% year-on-year increase. In October, we began series production of a new high volume cylinder block and head for DAF and, in November, we announced the ongoing series production of exhaust components in China. Together, these two new orders have the potential to provide a 25~30% growth beyond September’s 750,000 Engine Equivalent base. But despite these positive developments, the SinterCast share has declined.

As we mentioned in our 3Q Interim Report, it is inevitable that the global economic crisis will affect SinterCast, both in the customer market and in the share market. The most recent “Automotive Stock Watch”, published by Automotive News Europe and PricewaterhouseCoopers on 8 December 2008 shows that, on average, the shares of the survey’s regularly followed group of 15 representative automotive suppliers are down by 72% from their 12-month highs. The ‘best’ performer is down by 52% and the worst is down by 100%. Eight of the 15 are down by more than 66%. SinterCast is neither unique nor immune.

Although there have been many published opinions about the global economy and the automotive prognosis for 2009 and 2010, the truth is that nobody knows how the crisis will evolve and how/when it will recover. The CEO’s of many major OEMs have declined to comment on 2009/10 volumes stating that it would be “dishonest” or “irresponsible” to provide public projections at this time. We agree with this position. Certainly, if the OEMs do not yet know their volumes, it is not possible for SinterCast to know more. This also applies to the questions that we have received regarding the Company’s liquidity. At the moment, there are no plans to seek a new cash injection, but the cash position obviously depends on the length and depth of the downturn. We have an active Liquidity Protection Plan where we carefully and regularly review different market scenarios and adjust the expense side accordingly. Spending is limited to items required for the operation of the Company and the support of customers. The most professional thing that SinterCast can do is to monitor the development on a regular basis and to read-and-react in the best interest of the Company and its shareholders.

Throughout all of this, SinterCast has one important advantage. SinterCast is not a ‘normal’ supplier of automotive components. For the component or commodity suppliers, when the global market declines by x%, their revenues equally decline by x%. However, for SinterCast, many of our current programmes are still in the ramp-up phase and may be more vulnerable to a decreased growth rate rather than a volume reduction. And, for the new launches, even if the volumes may not be as high as originally expected, all new production provides incremental volumes.

Many shareholder e-mails have also suggested that more Press Releases would be helpful. With respect, we do not believe that this is appropriate. We will issue Press Releases when we receive new orders, but it is not our intention to issue general updates. General information won’t attract new investors to the Small Cap segment, and such Press Releases can also put the Company’s credibility at risk. We don’t believe that general updates will be helpful, and issuing such releases would take valuable time away from the most important focus – the business development.

SinterCast has established its technology and grown a strong business base. There is no need to change the strategy or the business model. However, like most companies, we are entering into a difficult 2009 and we will apply our experience and determination to navigate the best possible path for the Company.

The new Market Outlook section of the interim reports is intended to:

1. Provide a general overview of the potential market development,

2. Provide an indication of the total Engine Equivalent volume (and therefore, value) of the CGI programmes that SinterCast is currently involved in, and,

3. Show the progression of different programmes as they evolve from the “Development Pipeline” to the “Announced Programmes” and to the “Series Production” category.

In the automotive industry, virtually all powertrain programmes to be introduced before 2010 (the nearest 2-year period) are already decided and the launch dates are defined. The only questions are: when will SinterCast be allowed to publicly announce the programmes; and, how quickly will the production volume ramp-up? For ‘replacement’ engines, the ramp can be relatively fast while, for new engines, the ramp may depend on the sales success of the vehicles.

The 3~5 year period is a timeframe for which many programmes are under development, but the engines may not yet have received formal approval for series production. Even if the programmes are not yet approved for production, SinterCast is frequently aware of the OEM intentions. These programmes provide sufficient confidence to be included in the “Development Pipeline” category. SinterCast is also involved in development programmes beyond the 5-year horizon, but these are not generally included in the “Development Pipeline”. Some judgement (and estimation of mature volumes) is exercised in the definition of the “Development Pipeline”, but this reflects SinterCast’s best current knowledge.

New programmes will certainly be elevated into the “Current Series Production” category within the nearest 2-year period. For example, between the 22 August report and the 7 November report, the Hyundai 3.9 and 5.9 litre commercial vehicle programmes were elevated directly from the “Development Pipeline” to “Series Production” and the MAN 10.5 and 12.4 litre commercial vehicle programmes were elevated from “Announced Programmes” to “Series Production”.

While the last of the engine programmes that comprise the total volume of 5.5 million Engine Equivalents may take up to five years to begin production, and a further two years to ramp-up to mature volumes, new programmes will continuously be elevated into the “Series Production” category providing increased near-term revenue. At the same time, new programmes will continuously enter into the “Development Pipeline” to provide long-term growth.

Within SinterCast, we have frequently considered the opportunities to extend our technology to applications beyond CGI. However, until recently, we have always decided to apply all of our resources to the development of our CGI technology, customer production, and the development of the CGI market. Our objective has been to focus on one goal and to establish ourselves as the clear market leader.

Although there is still a lot of work and potential left in the development of the CGI market, our core CGI technology has been proven and it is highly respected within the foundry and automotive industries. We have succeeded to make the SinterCast name synonymous with CGI. From this foundation, we believe that we can now allocate some of our human resources toward the development of our thermal analysis technology for other materials.

As mentioned in the 2006 Full Year report published on 14 February, we have begun to evaluate the application of our thermal analysis know-how to the process control and quality control of ductile iron. A first patent has been filed and we hope to begin customer field trials during 2007. As ductile iron is the nearest metallurgical neighbour of CGI, and a demanding material that requires accurate foundry control, it is the logical starting point for the extension of our technology. Our initial discussions with the ductile iron foundry community have been well received and we will continue to work directly with the foundries in our attempt to develop a technology that meets their requirements.

SinterCast’s efforts in the CGI arena have earned widespread respect throughout the industry and have established SinterCast as the technology leader for thermal analysis. We will focus our future growth on our core thermal analysis competence and grow from within. If the intention of the question is to ask if we will ‘jump ship’ and begin to develop or acquire alternative products or technologies, the clear answer is ‘no’. Our CGI technology is successful and the high volume years now lie ahead of us, with production commitments representing almost 1 million Engine Equivalents per year already announced, and another 4 million Engine Equivalents per year under development. For SinterCast, this is precisely the wrong time to jump ship.

All legislation designed to improve fuel efficiency and to reduce CO2 emissions is helpful to SinterCast.

In the first instance, diesel engines have lower CO2 emissions than petrol engines. Therefore any legislation that requires lower CO2 output will also favour an increase in diesel production and sales. As the higher strength and stiffness of CGI is ideally suited to the higher thermal and mechanical leads found in diesel engines, the trend toward increased diesel sales should also positively influence the market demand for CGI.

Secondly, the improved properties of CGI allow diesel engines to operate at higher cylinder pressures. This, in turn, provides two benefits:

- Higher cylinder pressures enable smaller engines to provide performance levels that are similar to larger engines. For example, a 1.5 litre CGI engine may provide the same performance as a 2.0 litre grey iron or aluminium engine. The smaller CGI engines would provide 5-10% better fuel economy, and therefore, lower CO2 emissions.

- Higher cylinder pressures result in more complete combustion and therefore, less CO2 output. Even if the NOx emissions increase with higher cylinder temperatures and pressures, these can be eliminated by treating the exhaust gas. In this regard, it is positive for SinterCast that the EU focuses primarily on CO2.

Approximately 5 years ago, the association of European automobile manufacturers (ACEA) made a voluntary commitment to reduce CO2 emissions to 140 g/km by 2008. The primary strategy of the European OEMs was to convert petrol engine sales to diesels in order to meet the 140 g/km target. However, in the meantime, there has been an overall trend toward larger vehicles. The resulting demand for larger engines has increased fuel consumption and prevented the OEMs from meeting their voluntary CO2 target.

As it is now fairly certain that the European OEMs – who are currently at approximately 160 g/km – will not meet their voluntary target, the government is threatening to impose legislation. The prospect of government legislation in response to non-compliance with the voluntary target has been widely discussed in the automotive industry for the last 2-3 years, however, it is only recently that the media coverage has resulted in public awareness. In truth, a reduction to 120 g/km by 2012 is not significantly different from the self mandated target of 140 g/km due in 2008. What the OEMs are likely to seek is different CO2 levels for different clauses of vehicles, allowing the growing fraction of SUVs and large luxury vehicles to have higher CO2 limits.

Although it may not be popular with the OEMs or the public, more stringent emissions legislation and higher fuel prices will promote fuel efficiency, and this will always favour SinterCast’s long-term market opportunity.

It is true that the Sampling Cup shipments are a good general indicator of growth. However, it is difficult to establish a direct correlation between Sampling Cup shipments and the CGI series production volume. The reason for this is that customers frequently include large quantities of Sampling Cups together with the initial order for a new System 2000 installation. The bulk order ensures that the foundry will have start-up stocks and will not need to concern themselves with logistics and shipping costs for smaller orders, particularly for foundries located far from Sweden.

Another important consideration is that some countries have favourable import tax conditions for new equipment, in order to promote and support the development of the domestic manufacturing sector. These taxation policies encourage foundries to order larger quantities of Sampling Cups together with the initial installation rather than making separate orders of consumables in the future - at a higher tax rate. In this way, the Sampling Cup shipments during early 2006 were positively impacted by the new System 2000 installation in China (Q1) and the Mini-System 2000 installation in Korea (Q2). In contrast, the Sampling Cup shipments during 3Q06 were entirely related to series production requirements.

While Sampling Cup shipments can indeed be a good indicator of growth, during the initial series production period, the total Sampling Cup shipments are still dependent on new installations. The primary difference between 2005 and 2006 is that five new installations were announced during 2005 while only two new installations have been realised thus far during 2006. The fact that the year-to-date revenues for 2006 are nevertheless effectively the same as for 2005 is entirely due to the increase in series production. This positive growth in the series production activities is evident by comparing the production rate stated in the 3Q05 Interim Report (250,000 Engine Equivalents) to the current rate of 400,000 Engine Equivalents stated in the 3Q06 Report. Beyond this 60% increase in the current series production, a comparison of the 3Q05 and 3Q06 reports also shows that the future production potential has increased from 3.5 million Engine Equivalents to 5 million Engine Equivalents. Each of these individual developments illustrate the positive development of SinterCast’s market activities.

The main University-Industry-Government project related to automotive materials is known as ‘MERA’ (Manufacturing Engineering Research Area). The primary focus of the MERA project is the optimisation of machining techniques for new materials, in order to increase the overall competitiveness of the Swedish automotive industry. Another important result of the MERA project will be to support a new generation of university graduates that can enter the industry and contribute with strong materials and manufacturing skills. More information about the MERA program can be found at www.vinnova.se/vinnova_templates/Page____10406.aspx

Under the larger MERA umbrella, there is a specific automotive materials project known as ‘Optima’. Optima includes a sub-project related to the machining of CGI. SinterCast is one of the industrial partners of the Optima project and Steve Wallace, Operations Director, is a member of the Steering Group for the CGI sub-project. SinterCast will primarily contribute by supporting the production of various CGI components and test pieces for the machining trials. Additional information about the Optima project can be found at www.chalmers.se/mmt/SV/centra/projekt (Swedish only).

Another recent University-Industry-Government development was the formation of the Castings Innovation Centre (CIC). The CIC was formed in 2004 following an agreement between Gjuteriföreningen and Ingenjörshogskolan in Jönköping. The CIC is currently creating an “Industry Excellence Centre” with the CIC. The Industry Excellence Centre focuses on casting technology and is funded by the Swedish government and industry partners. SinterCast is one of the industrial partners of the Industry Excellence Centre, again providing technical contributions to projects related to CGI.

SinterCast is actively involved in research projects that can promote the overall development, awareness and acceptance of CGI. We are also committed to supporting the development of a new generation of engineering graduates that can further advance the global leadership and respect for Swedish metallurgical know-how and products.

The information strategies of the OEMs have an important influence on SinterCast’s ability to inform the market of its current development activities and the overall CGI market potential. In this regard, we welcome the early CGI announcements from International and GM.

In the case of International, the CGI ‘Big Bore’ information was released in parallel with two other announcements: the collaboration with MAN in Germany for heavy duty diesel engines; and, the introduction of the new International ProStarTM truck series that will use the Big Bore engines. The 11 and 13 litre Big Bore engines were said to be based on the MAN D20 and D26 CGI cylinder blocks, with modified fuel delivery and emissions systems to satisfy the more stringent US emissions legislations. The commitment to CGI increases the overall CGI market and provides a growth opportunity for SinterCast, especially in consideration of our existing production agreement to supply the MAN D20 CGI cylinder block at the Tupy foundry.

The new General Motors V8 diesel engine, based on a CGI cylinder block, was announced three years ahead of the series production launch. This pro-active announcement by GM is an important indicator of the continually escalating interest in diesel engines in America. The fact that GM specifically referred to CGI also indicates GM’s intention to present itself as a diesel leader in North America and shows the high-tech image the CGI has garnered in the industry. It is also interesting to note that, on 26 July 2006, Cummins announced a new V-diesel engine for the North American pick-up truck market. Although Cummins did not specifically refer to the cylinder block material, the announcement does reinforce the US diesel trend, and therefore, the increased market opportunity for CGI and SinterCast.

Overall, the recent announcements from International and GM demonstrate the need for CGI in advanced diesel engines, the trend toward diesels in North America, and thus the future growth of potential CGI. SinterCast continues to promote and support new CGI programs worldwide. Based on our industry leading technology, know-how, and foundry penetration, we will reap the benefit of the growing CGI market.

All car and truck companies try to maximise the commonality of their components in order to improve their economy of scale. While it is generally possible to commonise fuel delivery systems, hydraulic components, emissions assemblies and electronics over a wide range of engines, the cylinder block serves as the foundation of the engine and is therefore less flexible. The main criteria for the use of common cylinder blocks is that the engines must have the same centre-to-centre distance between the cylinder bores and the same number of cylinders. In the case of V-engines, the bank angle must also be the same.

In the present case, the MAN D08 is a family of 4 and 6 cylinder engines with 4.5-6.8 litre displacement and 150-225 horsepower. In contrast, the D20 and D26 engines are both 6-cylinder engines with a larger bore diameter, higher displacement (10.5 litres for the D20 and 12.4 litres for the D26) and higher horsepower (400-550 horsepower). While the differences between the D08 and the initial SinterCast-CGI D20 engines are too large to allow for a common cylinder block, the D26 engine will indeed be based on the D20 CGI cylinder block. As the D26 engines enter the market and the production volumes ramp-up, the combined D20 and D26 volume will provide “opportunities for future volume increases”, beyond the initial 20,000 cylinder block commitment, as indicated in the 18 August SinterCast-Tupy press release. As always, the task for SinterCast and Tupy is to provide a high quality and cost-effective CGI product and service in order to maximise our share of the production volume.

It is correct that the turnover for the April-June 2006 period has decreased slightly compared to 2005, from SEK 4.5 million (2005) to SEK 4.3 million (2006). However, in consideration of the positive market development and other external circumstances, we do not regard this as a negative result. The main reasons for our positive assessment are summarised as follows:

- Installations: New installations continue to be the most significant single item in determining the quarterly results. During 2Q06, the only installation revenue was from the Doosan Mini-System 2000. In contrast, higher revenues were received for the larger Hyundai full System 2000 installations during the same period 2005. Quarter-to-quarter results will continue to be influenced by the timing of new installations. Our focus is not on the individual timing, but rather on the positive long-term trend.

- Series Production: The continued increase in series production during the period effectively off-set the lower installation revenues. The increased production is evident from the increase in Sampling Cup shipments (20,100 units shipped during the first-half of 2006 vs. 12,200 during the first-half of 2005, +65%). The series production continues to develop positively.

- New Production: The start of series production of the Ford 3.6 litre V8 during April 2006 will provide additional production revenues as the volumes ramp-up. Likewise, production of the Ford-Otosan 7.3 litre commercial vehicle engine and the Hyundai V6 will begin soon and contribute to the remaining 2006 turnover. The new MAN 10.5 litre commercial vehicle order will also start series production during mid-2007, but initial revenues from pre-production activities and Engineering Support will be realised from 4Q06. As in the past, new orders will continue to be received, increasing the overall potential.

- Exchange Rates: The decline of the US dollar effectively reduced the consolidated revenue by SEK 0.5 million. In an apples-to-apples comparison of the 2Q06 and 2Q05 turnover, under the assumption of constant exchange rates, the April-June 2006 turnover was actually 20% higher than the same period 2005. The funds are primarily used to cover local expenses, so this is primarily a consolidation effect rather than a direct realised cash loss.

The overall business activities continues to develop positively. SinterCast’s primary focus remains on the cashflow result and, in this regard, the burn-rate for the April-June 2006 period was only SEK 0.8 million (liquidity reduced from MSEK 18.4 to MSEK 17.6). This good progress shows that the liquidity is secure as new production orders are received and production revenues continue to increase.

The Operating Result breakdown reflects the net result of SinterCast’s local expenses and local revenues in the three main geographical sectors. As a Swedish company, with R&D, production, engineering service and administration based in Katrineholm and commercial support provided from London, the vast majority of our operating expenses are based in Europe. Even when our engineering resources or sales efforts are applied to a project in Asia or the Americas, the personnel and R&D expenses are allocated to Europe – where the people are based and where the expenses are incurred.

SinterCast provides a result breakdown for Europe, Asia and the Americas in order to comply with reporting requirements. However, this reporting requirement is more relevant to the larger multinational companies that have local organisations to support their local business activities. As long as SinterCast continues to consolidate its technical activities and resources in Katrineholm, and use Katrineholm-based personnel to support worldwide customer activities, it will not be realistic to only balance the European expenses against the European revenues. For SinterCast, it is more appropriate to consider the Group result rather than the individual geographical sectors.

In general, the CGI specifications for passenger vehicle or commercial vehicle cylinder blocks and heads are the same. CGI is formally defined as having 0-20% nodularity which, in practice, corresponds to a stable production range of approximately ± 0.004% magnesium. Also, as cylinder heads incur higher thermal loading than cylinder blocks, it is preferable to produce the heads in the low-nodularity region (<10%) to optimise the heat transfer. This provides an advantage for the SinterCast technology as the patented magnesium fade simulation allows the SinterCast foundries to safely operate in the low-nodularity region without the risk of flake graphite formation.

The use of CGI for cylinder heads is initially included in the second wave of the Five Wave scenario, and also as a potential sixth step. Initially, in the second wave, CGI will be applied to commercial vehicle cylinder heads in the 8-20 litre size class. These large engines have high combustion temperatures and forces, and large cylinder bore diameters that require stiff heads that can span the bore without deformation. In the potential sixth step, CGI may also be applied to diesel engine cylinder heads for passenger vehicles where the continuous increase in loading threatens to exceed the durability limit of the current aluminium heads.